Let me start with a disclaimer – I’m not a credit card expert, financial advisor, or someone who’s spent years studying the intricate details of reward programs. I’m just a regular person who’s been using credit cards since 2021 and has stumbled through the learning process of figuring out what actually works for my lifestyle and spending patterns.

What I call my “smart wallet” is essentially my personal system of three credit cards that I’ve settled on after some trial and error. When I say “smart,” I don’t mean I’ve cracked some secret code or found loopholes that banks hate. I simply mean I’ve found a combination that gives me decent returns on money I’m already spending, without the hassle of managing too many cards or chasing rewards I’ll never actually use.

This article is purely about my personal experience – why I chose these specific cards, how I use them, and what kind of returns I’m seeing. Your spending habits, lifestyle, and financial goals are probably different from mine, so what works for me might not work for you. But maybe sharing my journey will give you some ideas for optimizing your own wallet.

How It All Started

Back in 2021, I was pretty much a credit card novice. I had a HDFC bank account for my business, and during one of those routine calls where they try to sell you everything, the representative mentioned I could get their Business Moneyback credit card for free. No joining fee, no annual fee for the first year – it seemed like a no-brainer.

That HDFC Business Moneyback was my introduction to the world of credit cards. I started noticing the cashback trickling in, began paying attention to reward categories, and slowly realized there might be more to this whole credit card game than I initially thought.

But as my spending patterns evolved, I realized that one card wasn’t going to cut it. Different cards excel in different areas, and trying to maximize rewards with just one card felt like leaving money on the table. That’s when I started researching and eventually switched to what I now call my smart wallet setup.

My Current Smart Wallet Setup

I’ve settled on a three-card system that covers all my bases without getting too complicated. Each card serves a specific purpose, and together they give me decent rewards across different spending categories while minimizing the hassle of managing too many accounts.

Here’s how my smart wallet breaks down:

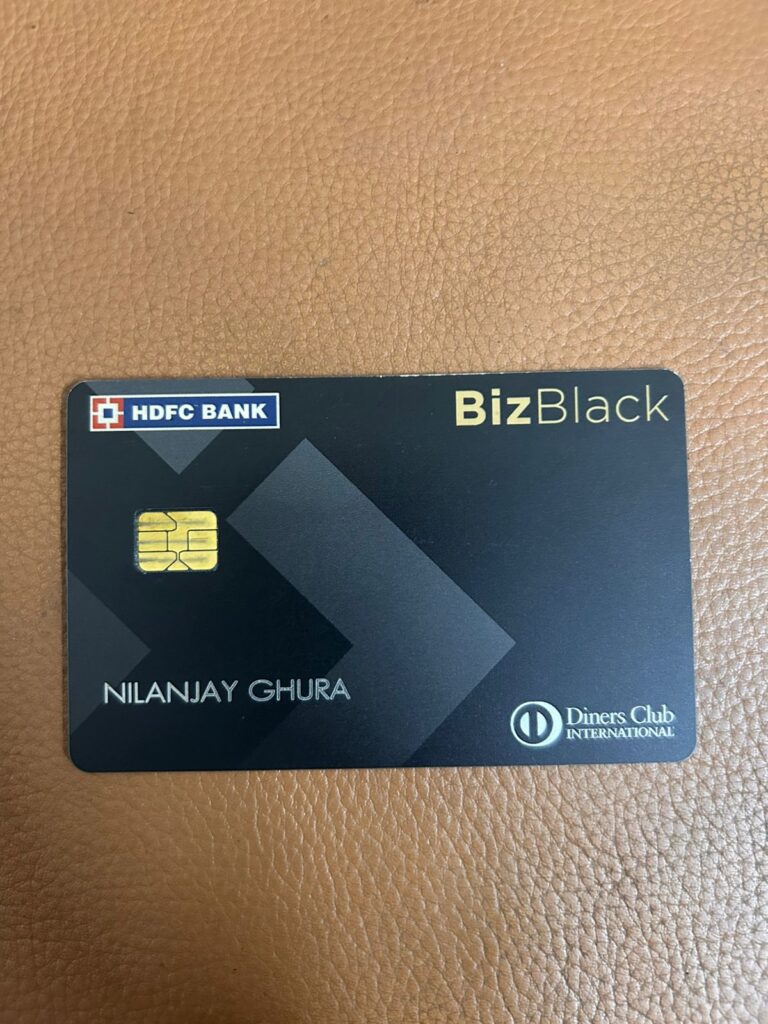

HDFC Biz Black Diners Club: My Business Workhorse

This card came as an upgrade from my previous HDFC Business Card, and it’s become the backbone of my business spending strategy. I use it primarily for business transactions, travel bookings, and even paying my income tax dues – and here’s why that makes sense.

The reward structure is straightforward: every INR 30 I spend gives me 1 reward point, and each point equals 1 rupee on the HDFC SmartBuy Portal. That’s essentially a 3.33% return rate, which is pretty solid for a business card. But where this card really shines is in the bonus categories.

When I book flights or hotels through MakeMyTrip using this card, I get 5-10X reward points. Since I travel to Spain frequently for work, this adds up quickly. Plus, here’s a neat hack I discovered: I have an HDFC Forex Prepaid Card for my Spain trips, and every time I add money to that Forex card using my HDFC Biz Black, I get 5X reward points. It’s like getting rewarded for preparing for my international travel.

One thing I really appreciate is that this card rewards me for paying income tax – not many credit cards do that. On average, I spend about INR 20,000 monthly on this card (excluding travel bookings), and the rewards keep accumulating nicely.

The unlimited domestic and international lounge access in India is a nice bonus, though I’ll admit the international lounge network outside India isn’t as extensive as I’d like.

The main downside? Diners Club isn’t accepted everywhere like Visa or Mastercard. You’ll run into places that just don’t take it, which is why having backup options is essential.

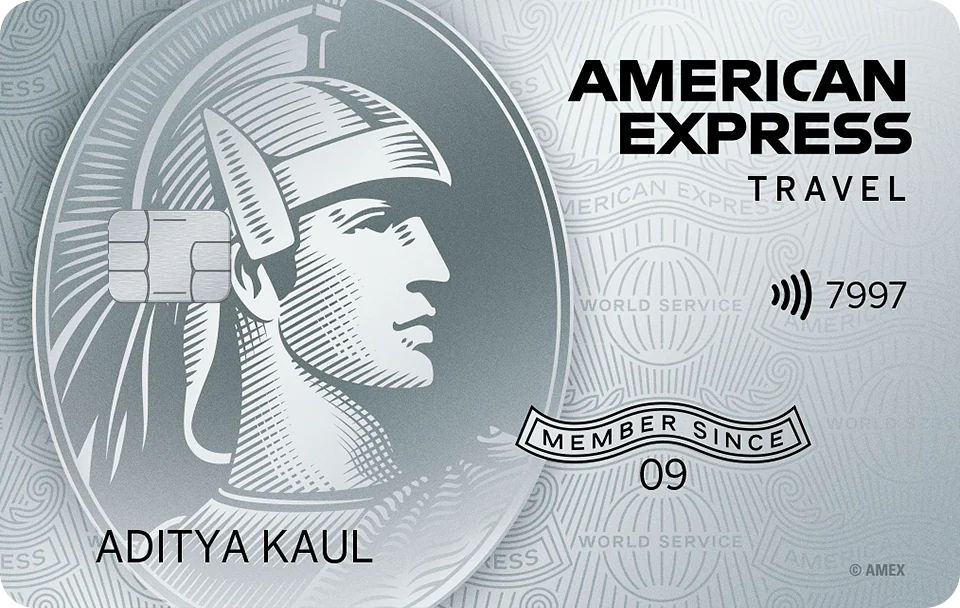

American Express Platinum Travel: My Personal Rewards Engine

I actually discovered this card by accident at Mumbai airport – I’d always wanted an Amex because of the brand reputation, but I didn’t know much about Platinum Travel specifically. It wasn’t until months later, after attending a credit card webinar, that I realized just how rewarding this card could be.

My strategy with this card is pretty specific: I use it exclusively for personal expenses, and I’ve developed what I call my “Amazon ecosystem hack.” Every month, I buy INR 10,000 worth of Amazon gift cards through the Gyfter platform, which gives me 3X reward points. I then add these gift cards to my Amazon Pay balance and use that balance for payments across Swiggy, Zomato, Amazon purchases, and pretty much anywhere that accepts Amazon Pay.

Gyfter limits you to INR 10,000 in gift card purchases per month, so I’ve made it a ritual to buy them at the beginning of each month. This gives me a guaranteed 3X return on money I’m going to spend anyway.

But the real magic happens with the milestone rewards. The Amex Platinum Travel is milestone-based, and I target the INR 1.9 lakh spending milestone, which gives me 7,500 + 7,500 bonus points on top of my regular spending points. That’s a significant bonus that makes the higher spending worthwhile.

What makes these points even more valuable is the 1:1 conversion ratio to Marriott hotel points. Being able to convert credit card points directly to hotel stays eases the trip budget.

Scapia Federal Credit Card: The UPI Game Changer

This is my newest addition, added in 2025 after hearing about it on The Great Indian Points and Miles Show. What attracted me wasn’t necessarily the rewards program, but a very specific feature: it’s a 2-in-1 card with both Visa and RuPay, and you get it with zero fees.

And the RuPay version allows me to make UPI transactions using a credit card.

This card fills a crucial gap in my wallet because there are plenty of situations where neither Diners Club nor Amex is accepted, but UPI and VISA are universally accepted in India.

My goal with this card is simple – use it for expenses where I don’t have the option to pay with my HDFC or Amex cards. I try to keep my spending under INR 15,000 monthly on this card.

The airport benefits are impressive too. The card offers complimentary dining, retail shopping and spa services across selected airports across India, along with unlimited access to airport lounges (which only gets activated when you spend either 10K INR on VISA card or 15K INR on Rupay card)

This card isn’t about maximizing rewards for me – it’s about convenience and filling the gaps where my other cards don’t work plus get some additional airport benefits.

If you would like to apply for this card, you can use my referral link: click here (If you activate the card, both me and you will get 1,000 Scapia points)

The Strategy Behind My Smart Wallet

Having three credit cards might seem like overkill, but there’s actually a method to this madness. Each card fills a specific role, and together they create a system where I’m almost always using the optimal card for any given transaction.

Here’s my mental framework for deciding which card to pull out:

Business expenses, travel bookings, and tax payments? HDFC Biz Black all the way. The 3.33% base return rate is solid, but the 5-10X multipliers on travel bookings through MakeMyTrip make this a no-brainer for work/personal travel. Plus, getting rewarded for paying income tax feels like finding free money.

Personal expenses where I want maximum rewards? American Express Platinum Travel, but specifically through my Amazon gift card strategy. By routing my personal spending through Amazon Pay, I’m essentially getting 3X points on purchases that would otherwise earn standard rates.

Everywhere else where the other two don’t work? That’s where Scapia shines. Small local vendors who only take UPI, places that don’t accept Diners Club or Amex, or situations where I just need the convenience of universal acceptance.

My monthly spending breakdown looks roughly like this:

- HDFC Biz Black: INR 20,000+ (business expenses, travel, tax payments)

- Amex Platinum Travel: INR 10,000 (Amazon gift cards for personal spending)

- Scapia Federal: Under INR 15,000 (gap-filling transactions)

This gives me a total monthly credit card spend of around INR 45,000, which might sound like a lot, but remember – this isn’t additional spending. This is money I was going to spend anyway, just routed through the most rewarding channels.

The learning curve and mistakes I made:

Initially, I tried to maximize rewards on every single transaction, which was exhausting. I’d stand at checkout counters trying to remember which card gave better rewards for groceries versus fuel versus dining. That approach was unsustainable.

The breakthrough came when I realized that having a clear purpose for each card was more important than chasing the absolute maximum rewards. Once I assigned specific roles – business card, personal rewards card, and gap-filler card – the decision-making became automatic.

Another mistake was not paying attention to acceptance networks early on. I learned the hard way that having the world’s best rewards card doesn’t help if you can’t actually use it where you need to shop. That’s why having both premium cards (HDFC, Amex) and a widely accepted backup (Scapia with Visa/RuPay) is crucial.

The milestone-based nature of the Amex card taught me the importance of consistent spending patterns. Rather than sporadic large purchases, I now plan my spending to hit those milestone bonuses systematically – like my monthly Amazon gift card purchases.

Is a Three-Card Smart Wallet Worth It?

After using this three-card system for a while now, here’s my honest assessment: yes, it works, but it’s not for everyone.

What I’ve learned that might help you:

The sweet spot isn’t about having the most cards or chasing every possible reward. It’s about finding cards that complement each other and match your actual spending patterns. My HDFC card handles business and travel, Amex maximizes my personal spending through the Amazon ecosystem, and Scapia fills the gaps where the other two can’t reach.

The key is having a clear purpose for each card. When I stopped trying to optimize every transaction and instead assigned specific roles to each card, managing them became effortless. Business expenses automatically go to HDFC, personal spending gets the Amex treatment, and everything else defaults to Scapia.

The numbers that matter:

With my current spending of roughly INR 45,000 monthly across all three cards, I’m generating meaningful returns without overthinking individual purchases. The HDFC card’s 3.33% base rate plus travel multipliers, Amex’s milestone bonuses, and Scapia’s convenience factor create a system that just works.

Is this complexity worth it for you?

Honestly, it depends on your spending habits and tolerance for managing multiple accounts. If you’re someone who travels frequently, has both business and personal expenses, and doesn’t mind the administrative overhead of tracking different reward systems, then yes – this approach can be quite rewarding.

But if you prefer simplicity and don’t want to think about which card to use when, you might be better off with just one or two really good cards that cover your primary spending categories.

Remember: I’m not a credit card expert, just someone sharing what works for my specific situation. Your spending patterns, travel frequency, and financial goals are probably different from mine. The best smart wallet is the one that fits your lifestyle, not necessarily the one with the highest theoretical returns.

The most important lesson I’ve learned is that the perfect credit card strategy is the one you’ll actually stick to consistently. Whether that’s one card or five cards, the key is finding a system that rewards your natural spending habits without turning every purchase into a complex decision.

What works for me might not work for you, and that’s perfectly fine. The goal isn’t to copy someone else’s wallet – it’s to build one that makes sense for your life.