If you read my Smart Wallet article from 2025 , you already know I’m a bit obsessed with optimizing my credit card setup. Not in a “chase every reward point” kind of way, but more in a “get decent returns without making it my full-time job” kind of way.

Well, it’s 2026 now, and I wanted to share an update on my credit card strategy—what’s working, what’s changed, and the actual returns I’m seeing.

Quick Recap: My 2025 Setup

Last year, my core wallet consisted of three cards:

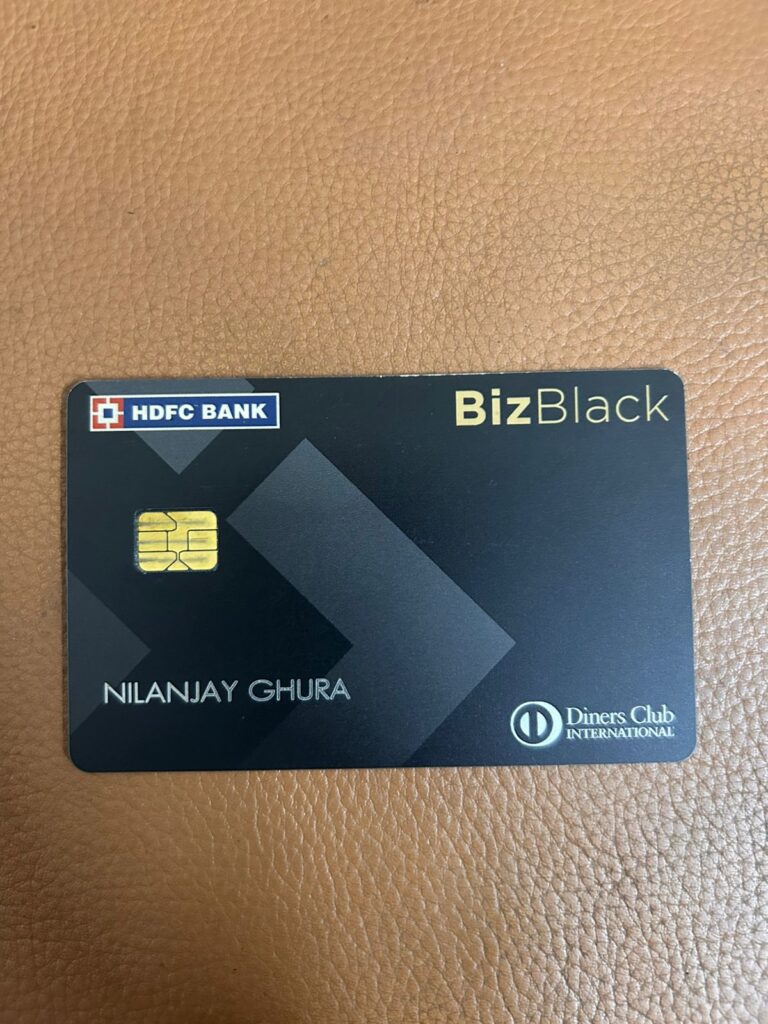

HDFC BizBlack Diners Club – My business workhorse for taxes, utility bills, and travel bookings. Fun fact: I got this as a free upgrade back in 2022 or 2023, so I don’t pay any annual fees. Lucky me.

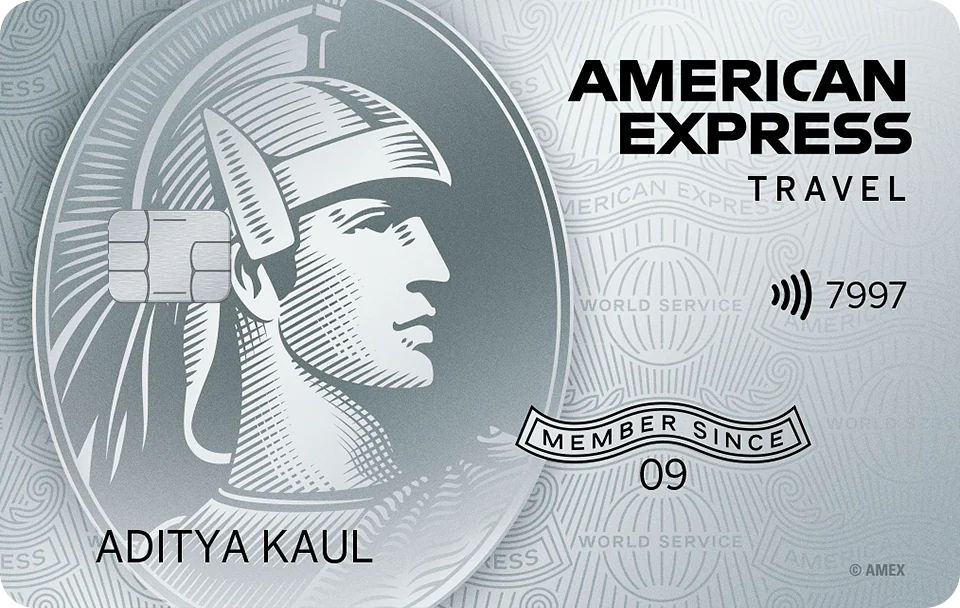

American Express Platinum Travel – This one came into my life by accident at Mumbai airport. I’ve always wanted an Amex card, and Platinum Travel is what they offered me. No regrets.

Scapia Federal – The new addition in Q4 2025. Dual functionality with both Visa and RuPay, which means I can pay via UPI using a credit card. That alone sold me.

These three cards formed my core strategy, and they did their job well.

The Numbers: How Much Did I Actually Earn?

Let me get straight to the good stuff—the returns.

2024 Performance:

- HDFC BizBlack: 8% return on spend

- Amex Platinum Travel: 7% return on spend

- Axis Atlas: 4% return on spend (RIP, I cancelled this card because I didn’t know how to use it properly back then)

- Average ROS: 6%

2025 Performance:

- HDFC BizBlack: 7% return on spend

- Amex Platinum Travel: 7% return on spend

- Scapia Federal: 8% return on spend

- Average ROS: 7%

That’s a 1% year-on-year growth. Not earth-shattering, but consistent improvement is what I’m after.

Breaking Down Each Card: How I Use Them in 2026

Let me walk you through my strategy for each card and why they’re still in my wallet.

Amex Platinum Travel: The Hotel Redemption Machine

This card has one main job for me: hotel stays.

Here’s how I use it:

Gyftr Vouchers for 3X Points – Every month, I buy Amazon Pay gift cards through Gyftr, which gives me 3X reward points. I then use those gift cards to pay for Uber, Amazon purchases, and anything else that accepts Amazon Pay.

Milestone Benefits – Amex Platinum Travel is milestone-based. If you hit certain spending thresholds, you get bonus points. The first milestone gives you 7500 + 7500 bonus points and second milestone is INR 4 lakh spends, which gives you 10,000 + 10,000 bonus points

Marriott Bonvoy Conversions – The real magic happens here. I will be converting my Amex points to Marriott Bonvoy points at a 1:1 ratio to book luxury hotel stays. Whether it’s a vacation or a work trip, this is my go-to redemption method.

Etihad Airways (Backup Redemption) – I’m a big fan of Etihad, and if I’m getting a good deal on flight bookings, I can convert Amex points to Etihad points at a 2:1 ratio. It’s not my primary use, but it’s a solid backup option.

HDFC BizBlack: The Business Powerhouse

This is purely a business card for me. If it’s related to work, it goes on this card.

What I Use It For:

- Tax payments (GST, income tax)

- Utility bills (office internet, Wi-Fi, phone subscriptions)

- Any other business-related expenses

Bonus Points Hack – If you spend at least INR 50,000 monthly on applicable transactions, you get an additional 7,500 points. That’s free money for spending I was going to do anyway.

HDFC SmartBuy Portal – The best part about this card is that I don’t always need to transfer points to partner programs. HDFC’s SmartBuy portal lets me redeem points directly for flight tickets, train bookings, shopping vouchers, and more. If I’m getting a better deal there, I skip the transfers entirely.

Scapia Federal: The UPI Game Changer

This is my newest addition, and it fills a very specific gap in my wallet.

Why I Got It:

- Dual functionality – Visa + RuPay in one card, which means I can pay via UPI using a credit card.

- Universal acceptance – When Amex or Diners Club isn’t accepted (which happens more often than you’d think), Scapia has my back.

Milestone Benefits – Scapia also has a monthly spending threshold. If you spend INR 20,000 monthly (across UPI, Visa, or both combined), you unlock domestic airport privileges. It used to be INR 10,000 on Visa or INR 15,000 on RuPay separately, but now they’ve clubbed it together.

The Downside – The redemption ratio is pretty bad. You can only redeem points on the Scapia app, and it’s at a 5:1 ratio (5 Scapia points = 1 rupee). Not great, but I mainly use this card for convenience and airport perks, not reward maximization.

The “Perk Only” Cards: HDFC Swiggy & Marriott Bonvoy

I also have two additional cards that I don’t use for regular spending. These are purely for perks.

HDFC Swiggy – I got this card for one reason: 12 months of Swiggy One membership. That’s it. I don’t use it for anything else.

HDFC Marriott Bonvoy – This card gives me silver status on Marriott Bonvoy, plus one free night worth 15,000 points at any Marriott property. Not a bad deal for INR 5,000 annual fees.

My 2026 Strategy: Staying the Course

For Q1 2026, my core stack remains the same:

- Amex Platinum Travel – Hit milestones, buy Gyftr vouchers and use reward points for hotel redemptions

- HDFC BizBlack – Business expenses and booking air/train tickets via Smartbuy portal.

- Scapia Federal – UPI payments and gap-filling transactions

I’m sticking with these three because they work. They complement each other without overlapping, and they cover almost every spending scenario I run into.

At the end of the year, I’ll track my returns again and see if I’ve maintained that 7% average—or maybe even pushed it higher. But for now, I’m not changing anything.

Final Thoughts

Credit card strategies don’t need to be complicated. You don’t need 10 cards or a PhD in reward programs. You just need a few cards that work well together and match your actual spending patterns.

For me, that’s three core cards and two perk cards. Simple, effective, and stress-free.

If you have your own credit card strategy or tips to share, drop them in the comments. I’m always curious to see what’s working for other people.

And if you’re just starting out with credit cards, remember: the goal isn’t to maximize every single rupee—it’s to build a system you can stick to without overthinking every purchase.

That’s the real win.